This article is part of the Multiple Imputation in Stata series. For a list of topics covered by this series, see the Introduction.

This article contains examples that illustrate some of the issues involved in using multiple imputation. Articles in the Multiple Imputation in Stata series refer to these examples, and more discussion of the principles involved can be found in those articles. However, it is possible to read this article independently, or to just read about the particular example that interests you (see the list of examples below).

These examples are not intended to test the validity of the techniques used or rigorously compare their effectiveness. However, they should give you some intuition about how they work and their strengths and weaknesses. Some of the simulation parameters (and occasionally the seed for the random number generator) were chosen in order to highlight the issue at hand, but none of them are atypical of real-world situations. The data are generated randomly from standard distributions in such a way that the "right" answers are known and you can see how closely different techniques approach those answers.

A Stata do file is provided for each example, along with commentary and selected output (in this web page). The do file also generates the data set used, with a set seed for reproducibility. Our suggestion is that you open the do file in Stata's do file editor or your favorite text editor and read it in parallel with the discussion in the article. Please note that the example do files are not intended to demonstrate the entire process of multiple imputation—they don't always check the fit or convergence of the imputation models, for example, which are very important things to do in real world use of multiple imputation.

Each example concludes with a "Lessons Learned" section, but we'd like to highlight one overall lesson: Multiple imputation can be a useful tool, but there are many ways to get it wrong and invalidate your results. Be very careful, and don't expect it to be quick and easy.

The examples are:

- Power

- MCAR vs. MAR vs. MNAR

- Imputing the Dependent Variable

- Non-Normal Data

- Transformations

- Non-Linearity

- Interactions

Power

The most common motivation for using multiple imputation is to try to increase the power of statistical tests by increasing the number of observations used (i.e. by not losing observations due to missing values). In our experience it rarely makes a large difference in practice. This example uses ideal circumstances to illustrate what extremely successful multiple imputation would look like.

Data

Observations: 1,000

Variables:

- x1-x10 drawn from standard normal distribution (independently)

- y is the sum of all x's, plus a normal error term

Missingness: Each value of the x variables has a 10% chance of being missing (MCAR).

Right Answers: Regressing y on all the x's, each x should have a coefficient of 1.

Procedure

Begin with complete cases analysis:

Source | SS df MS Number of obs = 369

-------------+------------------------------ F( 10, 358) = 6.71

Model | 3882.86207 10 388.286207 Prob > F = 0.0000

Residual | 20722.7734 358 57.884842 R-squared = 0.1578

-------------+------------------------------ Adj R-squared = 0.1343

Total | 24605.6355 368 66.86314 Root MSE = 7.6082

------------------------------------------------------------------------------

y | Coef. Std. Err. t P>|t| [95% Conf. Interval]

-------------+----------------------------------------------------------------

x1 | .733993 .4216582 1.74 0.083 -.0952453 1.563231

x2 | 1.664231 .3867292 4.30 0.000 .903684 2.424777

x3 | 1.51406 .3907875 3.87 0.000 .7455327 2.282588

x4 | .2801067 .395164 0.71 0.479 -.4970278 1.057241

x5 | .8524305 .4076557 2.09 0.037 .0507297 1.654131

x6 | .7704437 .413519 1.86 0.063 -.042788 1.583675

x7 | .6512155 .3938107 1.65 0.099 -.1232575 1.425689

x8 | .9173208 .3969585 2.31 0.021 .1366572 1.697984

x9 | .8736406 .4115488 2.12 0.034 .0642835 1.682998

x10 | .9222064 .4123417 2.24 0.026 .11129 1.733123

_cons | -.1999121 .3975523 -0.50 0.615 -.9817434 .5819192

------------------------------------------------------------------------------

Note that although each x value has just a 10% chance of being missing, because we have ten x variables per observation almost 2/3 of the observations are missing at least one value and must be dropped. As a result, the standard errors are quite large, and the coefficients on four of the ten x's are not significantly different from zero.

After multiple imputation, the same regression gives the following:

Multiple-imputation estimates Imputations = 10

Linear regression Number of obs = 1000

Average RVI = 0.1483

Largest FMI = 0.2356

Complete DF = 989

DF adjustment: Small sample DF: min = 142.63

avg = 425.17

max = 928.47

Model F test: Equal FMI F( 10, 802.0) = 18.13

Within VCE type: OLS Prob > F = 0.0000

------------------------------------------------------------------------------

y | Coef. Std. Err. t P>|t| [95% Conf. Interval]

-------------+----------------------------------------------------------------

x1 | .793598 .2679515 2.96 0.003 .2657743 1.321422

x2 | 1.133405 .2482047 4.57 0.000 .6460259 1.620785

x3 | 1.33182 .2521916 5.28 0.000 .8364684 1.827172

x4 | 1.159887 .2714759 4.27 0.000 .624309 1.695465

x5 | 1.181207 .2901044 4.07 0.000 .607747 1.754667

x6 | 1.305636 .2835268 4.60 0.000 .7466279 1.864645

x7 | .6258813 .2568191 2.44 0.015 .121268 1.130494

x8 | 1.143631 .253376 4.51 0.000 .6461328 1.64113

x9 | 1.112347 .2838261 3.92 0.000 .5520503 1.672644

x10 | 1.053309 .2612807 4.03 0.000 .5397648 1.566854

_cons | .0305628 .2499378 0.12 0.903 -.4599457 .5210712

------------------------------------------------------------------------------

The standard errors are much smaller than with complete cases analysis, and all of the coefficients are significantly different from zero. This illustrates the primary motivation for using multiple imputation.

Lessons Learned

This data set is ideal for multiple imputation because it has large numbers of observations with partial data. Complete cases analysis must discard all these observations. Multiple imputation can use the information they contain to improve the results.

Note that the imputation model could not do a very good job of predicting the missing values of the x's based on the observed data. The x's are completely independent of each other and thus have no predictive power. y has some but not much: if you regress each x on y and all the other x's (which is what the imputation model used does), the R-squared values are all less than 0.1 and most are less than 0.03. The success of multiple imputation does not depend on imputing the "right" values of the missing variables for individual observations, but rather on correctly modeling their distribution conditional on the observed data.

MCAR vs. MAR vs. MNAR

Whether your data are Missing Completely at Random (probability of being missing does not depend on either observed or unobserved data), Missing at Random (probability of being missing depends only on observed data), or Missing Not at Random (probability of being missing depends on unobserved data) is very important in deciding how to analyze it. This example shows how complete cases analysis and multiple imputation respond to different mechanisms for missingness.

Data

Observations: 1,000

Variables:

- x is drawn from standard normal distribution

- y is x plus a normal error term

Missingness:

- y is always observed

- First run: probability of x being missing is 10% for all observations (MCAR)

- Second run: probability of x being missing is proportional to y (MAR)

- Third run: probability of x being missing is proportional to x (MNAR)

Right Answers: Regressing y on x, x should have a coefficient of 1.

Procedure

We'll analyze this data set three times, once when it is MCAR, once when it is MAR, and once when it is MNAR.

MCAR

In the first run, the data set is MCAR and both complete cases analysis and multiple imputation give unbiased results.

Complete cases analysis:

Source | SS df MS Number of obs = 882

-------------+------------------------------ F( 1, 880) = 932.47

Model | 918.60551 1 918.60551 Prob > F = 0.0000

Residual | 866.913167 880 .985128598 R-squared = 0.5145

-------------+------------------------------ Adj R-squared = 0.5139

Total | 1785.51868 881 2.02669543 Root MSE = .99254

------------------------------------------------------------------------------

y | Coef. Std. Err. t P>|t| [95% Conf. Interval]

-------------+----------------------------------------------------------------

x | .9842461 .0322319 30.54 0.000 .9209858 1.047506

_cons | -.0481664 .0334249 -1.44 0.150 -.1137683 .0174354

------------------------------------------------------------------------------

Multiple imputation:

Multiple-imputation estimates Imputations = 10

Linear regression Number of obs = 1000

Average RVI = 0.1112

Largest FMI = 0.1583

Complete DF = 998

DF adjustment: Small sample DF: min = 262.51

avg = 541.98

max = 821.46

Model F test: Equal FMI F( 1, 821.5) = 1014.02

Within VCE type: OLS Prob > F = 0.0000

------------------------------------------------------------------------------

y | Coef. Std. Err. t P>|t| [95% Conf. Interval]

-------------+----------------------------------------------------------------

x | .9837383 .0308928 31.84 0.000 .9231003 1.044376

_cons | -.0377668 .0342445 -1.10 0.271 -.1051958 .0296621

------------------------------------------------------------------------------

MAR

Now, consider the case where the probability of x being missing is proportional to y (which is always observed), making the data MAR. With MAR data, complete cases analysis is biased:

Source | SS df MS Number of obs = 652

-------------+------------------------------ F( 1, 650) = 375.85

Model | 252.090968 1 252.090968 Prob > F = 0.0000

Residual | 435.966034 650 .670716976 R-squared = 0.3664

-------------+------------------------------ Adj R-squared = 0.3654

Total | 688.057002 651 1.0569232 Root MSE = .81897

------------------------------------------------------------------------------

y | Coef. Std. Err. t P>|t| [95% Conf. Interval]

-------------+----------------------------------------------------------------

x | .6857927 .035374 19.39 0.000 .6163317 .7552538

_cons | -.558313 .0352209 -15.85 0.000 -.6274736 -.4891525

------------------------------------------------------------------------------

However, multiple imputation gives unbiased estimates:

Multiple-imputation estimates Imputations = 10

Linear regression Number of obs = 1000

Average RVI = 0.4234

Largest FMI = 0.3335

Complete DF = 998

DF adjustment: Small sample DF: min = 78.63

avg = 90.20

max = 101.78

Model F test: Equal FMI F( 1, 78.6) = 750.78

Within VCE type: OLS Prob > F = 0.0000

------------------------------------------------------------------------------

y | Coef. Std. Err. t P>|t| [95% Conf. Interval]

-------------+----------------------------------------------------------------

x | .9909115 .0361642 27.40 0.000 .9189232 1.0629

_cons | -.0544014 .0366092 -1.49 0.140 -.1270175 .0182146

------------------------------------------------------------------------------

MNAR

Finally consider the case where the probability of x being missing proportional to x. This makes the data missing not at random (MNAR), and with MNAR data both complete cases analysis and multiple imputation are biased.

Complete cases analysis:

Source | SS df MS Number of obs = 679

-------------+------------------------------ F( 1, 677) = 463.29

Model | 464.94386 1 464.94386 Prob > F = 0.0000

Residual | 679.422756 677 1.00357866 R-squared = 0.4063

-------------+------------------------------ Adj R-squared = 0.4054

Total | 1144.36662 678 1.68785636 Root MSE = 1.0018

------------------------------------------------------------------------------

y | Coef. Std. Err. t P>|t| [95% Conf. Interval]

-------------+----------------------------------------------------------------

x | 1.093581 .0508074 21.52 0.000 .9938225 1.19334

_cons | .0420364 .0469578 0.90 0.371 -.050164 .1342368

------------------------------------------------------------------------------

Multiple imputation:

Multiple-imputation estimates Imputations = 10

Linear regression Number of obs = 1000

Average RVI = 0.3930

Largest FMI = 0.3425

Complete DF = 998

DF adjustment: Small sample DF: min = 74.96

avg = 144.00

max = 213.04

Model F test: Equal FMI F( 1, 75.0) = 561.03

Within VCE type: OLS Prob > F = 0.0000

------------------------------------------------------------------------------

y | Coef. Std. Err. t P>|t| [95% Conf. Interval]

-------------+----------------------------------------------------------------

x | 1.223772 .0516665 23.69 0.000 1.120846 1.326698

_cons | .3816984 .0402614 9.48 0.000 .3023366 .4610602

------------------------------------------------------------------------------

Complete cases analysis actually does better with this particular data set, but that's not true in general.

Lessons Learned

Always investigate whether your data set is plausibly MCAR or MAR. (For example, run logits on indicators of missingness and see if anything predicts it—if it does the data set is MAR rather than MCAR.) If your data set is MAR, consider using multiple imputation rather than complete cases analysis.

MNAR, by definition, cannot be detected by looking at the observed data. You'll have to think carefully about how the data was collected and consider whether some values of the variables might make the data more or less likely to be observed. Unfortunately, the options for working with MNAR data are limited.

Imputing the Dependent Variable

Many researchers believe it is inappropriate to use imputed values of the dependent variable in the analysis model, especially if the variables used in the imputation model are the same as the variables used in the analysis model. The thinking is that the imputed values add no information since they were generated using the model that is being analyzed.

Unfortunately, this sometimes is misunderstood as meaning that the dependent variable should not be included in the imputation model. That would be a major mistake.

Complete code for this example

Data

Observations: 1,000

Variables:

- x1-x3 drawn from standard normal distribution (independently)

- y is the sum of all x's, plus a normal error term

Missingness: y and x1-x3 have a 20% probability of being missing (MCAR).

Right Answers: Regressing y on x1-x3, the coefficient on each should be 1.

Procedure

The following are the results of complete cases analysis:

Source | SS df MS Number of obs = 4079

-------------+------------------------------ F( 3, 4075) = 3944.41

Model | 12264.8582 3 4088.28608 Prob > F = 0.0000

Residual | 4223.63457 4075 1.03647474 R-squared = 0.7438

-------------+------------------------------ Adj R-squared = 0.7437

Total | 16488.4928 4078 4.04327926 Root MSE = 1.0181

------------------------------------------------------------------------------

y | Coef. Std. Err. t P>|t| [95% Conf. Interval]

-------------+----------------------------------------------------------------

x1 | .9834974 .0160921 61.12 0.000 .9519481 1.015047

x2 | 1.000172 .0160265 62.41 0.000 .9687511 1.031593

x3 | 1.003089 .0159724 62.80 0.000 .9717744 1.034404

_cons | -.0003362 .0159445 -0.02 0.983 -.0315962 .0309238

------------------------------------------------------------------------------

If you leave y out of the imputation model, imputing only x1-x3, the coefficients on the x's in the final model are biased towards zero:

Multiple-imputation estimates Imputations = 10

Linear regression Number of obs = 7993

Average RVI = 0.4014

Largest FMI = 0.3666

Complete DF = 7989

DF adjustment: Small sample DF: min = 72.62

avg = 119.53

max = 161.84

Model F test: Equal FMI F( 3, 223.0) = 1761.75

Within VCE type: OLS Prob > F = 0.0000

------------------------------------------------------------------------------

y | Coef. Std. Err. t P>|t| [95% Conf. Interval]

-------------+----------------------------------------------------------------

x1 | .7946113 .0185175 42.91 0.000 .7580219 .8312007

x2 | .7983325 .0199962 39.92 0.000 .7584766 .8381885

x3 | .8001109 .0193738 41.30 0.000 .7616436 .8385782

_cons | .0041643 .0183891 0.23 0.821 -.0321492 .0404778

------------------------------------------------------------------------------

Why is that? An easy way to see the problem is to look at correlations. First, the correlation between y and x1 in the unimputed data:

| y x1

-------------+------------------

y | 1.0000

x1 | 0.5032 1.0000

Now, the correlation between y and x1 for those observations where x1 is imputed (this is calculated for the first imputation, but the others are similar):

| y x1

-------------+------------------

y | 1.0000

x1 | -0.0073 1.0000

Because y is not included in the imputation model, the imputation model creates values of x1 (and x2 and x3) which are not correlated with y. This does not match the observed data. It also biases the results of the final model by adding observations in which y really is unrelated to x1, x2, and x3.

This problem goes away if y is included in the imputation model. Given the nature of chained equations, this means that values of y must be imputed. However, you're under no obligation to use those values in your analysis model. Simply create an indicator variable for "y is missing in the observed data," which can be done automatically with misstable sum, gen(miss_), and then add if !miss_y to the regression command. This restricts the regression to those observations where y is actually observed, so any imputed values of y are not used. Here are the results:

Multiple-imputation estimates Imputations = 10

Linear regression Number of obs = 7993

Average RVI = 0.6402

Largest FMI = 0.5076

Complete DF = 7989

DF adjustment: Small sample DF: min = 38.27

avg = 82.39

max = 182.83

Model F test: Equal FMI F( 3, 137.9) = 4691.72

Within VCE type: OLS Prob > F = 0.0000

------------------------------------------------------------------------------

y | Coef. Std. Err. t P>|t| [95% Conf. Interval]

-------------+----------------------------------------------------------------

x1 | .9852388 .0150348 65.53 0.000 .9550372 1.01544

x2 | .9923264 .0158077 62.77 0.000 .9603327 1.02432

x3 | .9936324 .0129186 76.91 0.000 .9681437 1.019121

_cons | -.0015309 .0145755 -0.11 0.917 -.0306997 .0276378

------------------------------------------------------------------------------

On the other hand, using the imputed values of y turns out to make almost no difference in this case (see the complete code).

Lessons Learned

Always include the dependent variable in your imputation model. Whether you should use imputed values of the dependent variable in your analysis model is unclear, but always impute them.

Non-Normal Data

The obvious way to impute a continuous variable is regression (i.e. the regress command in mi impute chained). However, it applies a normal error term. What happens if a variable is not at all normally distributed?

Complete code for this example

Data

Observations: 10,000

Variables:

- g is a binary (1/0) variable with a 50% probability of being 1

- x is drawn from the standard normal distribution, then 5 is added if g is 1. Thus x is bimodal.

- y is x plus a normal error term

Missingness: Both y and x have a 10% probability of being missing (MCAR).

Right Answers: Regressing y on x, x should have a coefficient of 1.

Procedure

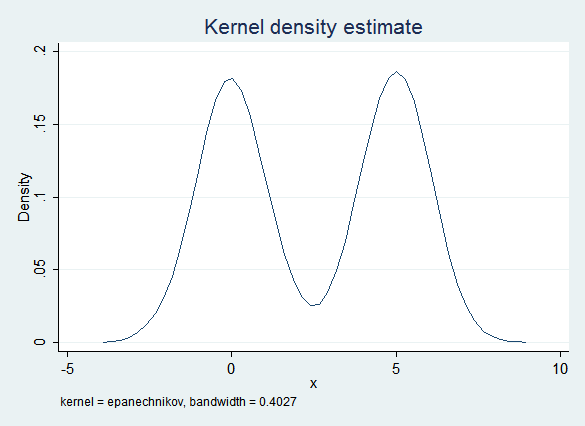

Given the way x was constructed, it has a bimodal distribution and is definitely not normal:

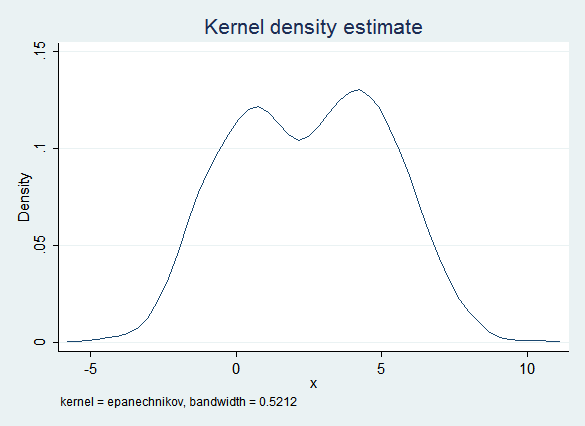

The obvious imputation model (regress x on y) captures some of this bimodality because of the influence of y. However, the error term is normal and does not take into account the non-normal distribution of the data. Thus this model is too likely to create imputed values that are near 2.5 (the "valley" between the two "peaks") and the distribution of the imputed data is "too normal":

However, the regression results are quite good:

Multiple-imputation estimates Imputations = 10

Linear regression Number of obs = 10000

Average RVI = 0.2471

Largest FMI = 0.1977

Complete DF = 9998

DF adjustment: Small sample DF: min = 238.92

avg = 414.68

max = 590.43

Model F test: Equal FMI F( 1, 590.4) = 63916.86

Within VCE type: OLS Prob > F = 0.0000

------------------------------------------------------------------------------

y | Coef. Std. Err. t P>|t| [95% Conf. Interval]

-------------+----------------------------------------------------------------

x | 1.001225 .0039603 252.82 0.000 .9934473 1.009003

_cons | -.0068119 .0152489 -0.45 0.655 -.0368514 .0232276

------------------------------------------------------------------------------

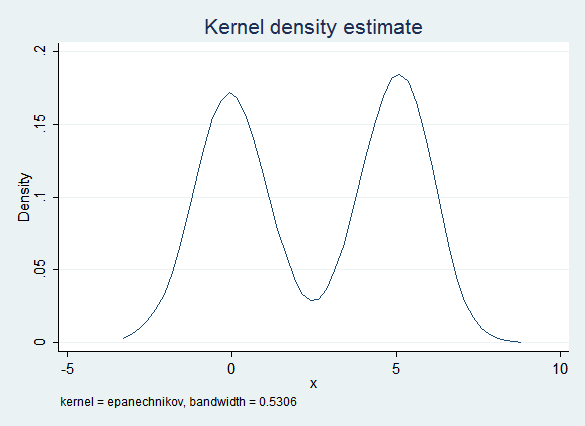

Replacing regression with Predictive Mean Matching gives a much better fit. PMM begins with regression, but it then finds the observed value of x that is the nearest match. Because there are fewer observed values in the "valley" PMM is less likely to find a match there, resulting in a distribution that is closer to the original:

Regression results after imputing with PMM are also good:

Multiple-imputation estimates Imputations = 10

Linear regression Number of obs = 10000

Average RVI = 0.2885

Largest FMI = 0.2698

Complete DF = 9998

DF adjustment: Small sample DF: min = 131.79

avg = 148.15

max = 164.50

Model F test: Equal FMI F( 1, 131.8) = 53733.02

Within VCE type: OLS Prob > F = 0.0000

------------------------------------------------------------------------------

y | Coef. Std. Err. t P>|t| [95% Conf. Interval]

-------------+----------------------------------------------------------------

x | .9976108 .0043037 231.80 0.000 .9890976 1.006124

_cons | .0105094 .0156034 0.67 0.502 -.0202993 .0413181

------------------------------------------------------------------------------

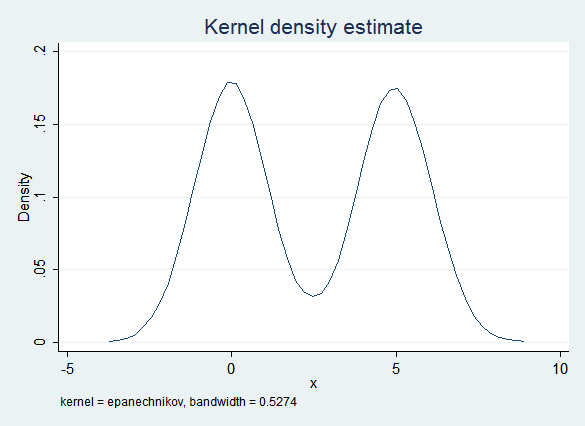

On the other hand, x is distributed normally within each g group. If you impute the two groups separately then ordinary regression fits the data quite well:

The regression results are also good:

Multiple-imputation estimates Imputations = 10

Linear regression Number of obs = 10000

Average RVI = 0.6503

Largest FMI = 0.4656

Complete DF = 9998

DF adjustment: Small sample DF: min = 45.53

avg = 63.49

max = 81.45

Model F test: Equal FMI F( 1, 81.4) = 48664.75

Within VCE type: OLS Prob > F = 0.0000

------------------------------------------------------------------------------

y | Coef. Std. Err. t P>|t| [95% Conf. Interval]

-------------+----------------------------------------------------------------

x | .9996345 .0045314 220.60 0.000 .9906191 1.00865

_cons | .0032657 .0183149 0.18 0.859 -.0336105 .0401419

------------------------------------------------------------------------------

Lessons Learned

PMM can be a very effective tool for imputing non-normal data. On the other hand, if you can identify groups whose data may vary in systematically different ways, consider imputing them separately.

However, the regression results were uniformly good, even when the data were imputed using the original regression model where the distribution of the imputed values didn't match the distribution of the observed values very well. In part this is because we had a large number of observations and a simple model, but in general the relationship between face validity and getting valid estimates using the imputed data is unclear.

Transformations

Given non-normal data, it's appealing to try to transform it in a way that makes it more normal. But what if the other variables in the model are related to the original values of the variable rather than the transformed values?

Complete code for this example

Data

Observations: 10,000

Variables:

- x1 is drawn from the standard normal distribution, then exponentiated. Thus it is log-normal

- x2 is drawn from the standard normal distribution

- y is the sum of x1, x2 and a normal error term

Missingness: x1, x2 and y have a 10% probability of being missing (MCAR)

Right Answers: Regressing y on x1 and x2, both should have a coefficient of 1.

Procedure

First, complete cases analysis for comparison. It does quite well, as we'd expect with MCAR data (and a simple model with lots of observations):

Source | SS df MS Number of obs = 7299

-------------+------------------------------ F( 2, 7296) =19024.33

Model | 38421.4045 2 19210.7023 Prob > F = 0.0000

Residual | 7367.47472 7296 1.00979643 R-squared = 0.8391

-------------+------------------------------ Adj R-squared = 0.8391

Total | 45788.8793 7298 6.27416816 Root MSE = 1.0049

------------------------------------------------------------------------------

y | Coef. Std. Err. t P>|t| [95% Conf. Interval]

-------------+----------------------------------------------------------------

x1 | 1.001594 .0057231 175.01 0.000 .9903751 1.012813

x2 | .9973623 .0117407 84.95 0.000 .9743471 1.020377

_cons | .0035444 .0149663 0.24 0.813 -.025794 .0328827

------------------------------------------------------------------------------

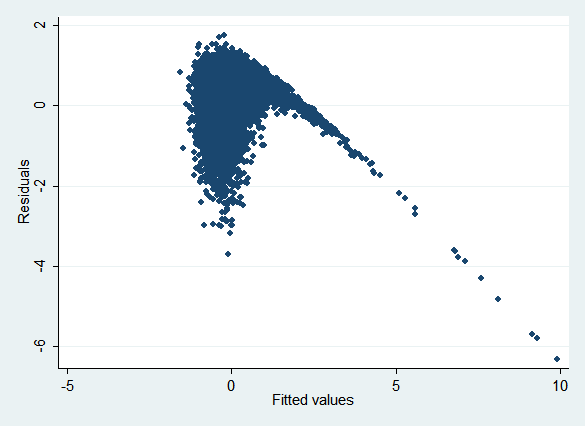

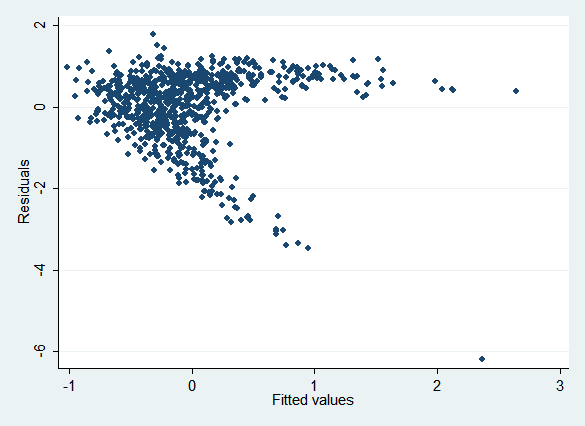

This data set presents a dilemma for imputation: x1 can be made normal simply by taking its log, but y is related to x1, not the log of x1. Regressing ln(x1) on x2 and y (as the obvious imputation model will do) results in the following plot of residuals vs. fitted values (rvfplot):

If the model were specified correctly, we'd expect the points to be randomly distributed around the y axis regardless of their x location. Clearly that's not the case.

The obvious way to impute this data would be to:

- Log transform x1 by creating lnx1 = ln(x1)

- Impute lnx1 using regression

- Create the passive variable ix1 = exp(lnx1) to reverse the transformation

Here are the regression results after doing so:

Multiple-imputation estimates Imputations = 10

Linear regression Number of obs = 10000

Average RVI = 196.4421

Largest FMI = 0.9987

Complete DF = 9997

DF adjustment: Small sample DF: min = 5.89

avg = 242.41

max = 701.09

Model F test: Equal FMI F( 2, 12.8) = 3.84

Within VCE type: OLS Prob > F = 0.0493

------------------------------------------------------------------------------

y | Coef. Std. Err. t P>|t| [95% Conf. Interval]

-------------+----------------------------------------------------------------

ix1 | .014417 .0213705 0.67 0.525 -.0381112 .0669452

x2 | .9951566 .0235333 42.29 0.000 .9489525 1.041361

_cons | 1.583044 .0384844 41.13 0.000 1.502835 1.663253

------------------------------------------------------------------------------

As you see, the coefficient on ix1 (imputed untransformed x1) is very strongly biased towards zero. Now try imputing lnx1 using Predictive Mean Matching rather than regression:

Multiple-imputation estimates Imputations = 10

Linear regression Number of obs = 10000

Average RVI = 0.7058

Largest FMI = 0.6292

Complete DF = 9997

DF adjustment: Small sample DF: min = 24.80

avg = 53.56

max = 74.84

Model F test: Equal FMI F( 2, 52.8) = 8286.63

Within VCE type: OLS Prob > F = 0.0000

------------------------------------------------------------------------------

y | Coef. Std. Err. t P>|t| [95% Conf. Interval]

-------------+----------------------------------------------------------------

ix1 | .9554301 .009311 102.61 0.000 .9362457 .9746144

x2 | .9537128 .0146582 65.06 0.000 .9245112 .9829144

_cons | .0843407 .0192948 4.37 0.000 .0457588 .1229226

------------------------------------------------------------------------------

Now both coefficients are biased towards zero, though not nearly as strongly.

What if we simply ignore the fact that x1 is not normally distributed and impute it directly? The results are actually better:

Multiple-imputation estimates Imputations = 10

Linear regression Number of obs = 10000

Average RVI = 0.3873

Largest FMI = 0.3401

Complete DF = 9997

DF adjustment: Small sample DF: min = 84.25

avg = 179.94

max = 337.16

Model F test: Equal FMI F( 2, 133.4) = 17538.58

Within VCE type: OLS Prob > F = 0.0000

------------------------------------------------------------------------------

y | Coef. Std. Err. t P>|t| [95% Conf. Interval]

-------------+----------------------------------------------------------------

x1 | .9980159 .0060605 164.68 0.000 .9859646 1.010067

x2 | .9912113 .0117879 84.09 0.000 .967869 1.014554

_cons | .0108679 .0140238 0.77 0.439 -.0167172 .038453

------------------------------------------------------------------------------

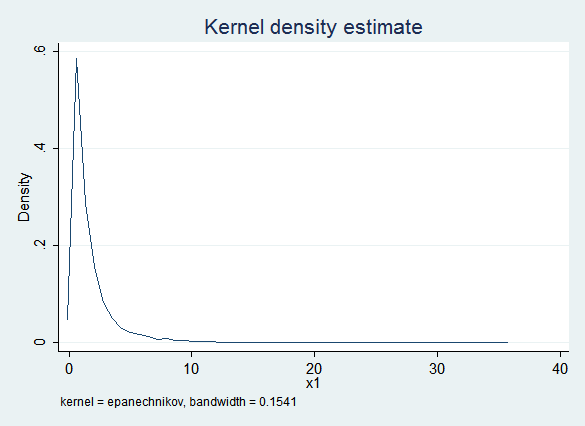

This clearly works well, but raises the question of face validity. Here is a kernel density plot of the observed values of x1:

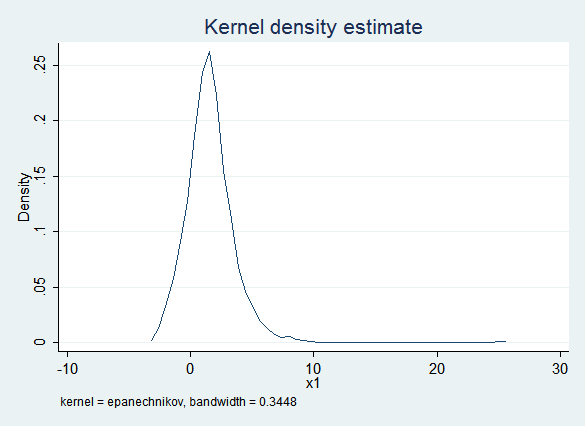

Here is a kernel density plot of the imputed values of x1:

The obvious problem is that the imputed values of x1 are frequently less than zero while the observed values of x1 are always positive. This would be especially problematic if you thought you might want to use a log transform later in the process.

Given the constraint that x1 cannot be less than zero, truncreg seems like a plausible alternative. Unfortunately, truncreg fails to converge for this data set (for reasons not yet clear to us). But PMM will also honor that constraint:

Here are the regression results with PMM:

Multiple-imputation estimates Imputations = 10

Linear regression Number of obs = 10000

Average RVI = 0.3702

Largest FMI = 0.3664

Complete DF = 9997

DF adjustment: Small sample DF: min = 72.89

avg = 147.11

max = 193.33

Model F test: Equal FMI F( 2, 145.1) = 17890.15

Within VCE type: OLS Prob > F = 0.0000

------------------------------------------------------------------------------

y | Coef. Std. Err. t P>|t| [95% Conf. Interval]

-------------+----------------------------------------------------------------

x1 | 1.000568 .0056325 177.64 0.000 .9894588 1.011677

x2 | .9977033 .012447 80.16 0.000 .9728958 1.022511

_cons | .009171 .014612 0.63 0.531 -.0196674 .0380094

------------------------------------------------------------------------------

Lessons Learned

The lesson of this example is not that you should never transform covariates. Keep in mind that what makes transforming x1 problematic in this example is that the relationship between y and x1 is known to be linear.

The real lesson is that misspecification in your imputation model can cause problems in your analysis model. Be sure to run the regressions implied by your imputation models separately and check them for misspecification. A secondary lesson is that PMM can work well for non-normal data.

Non-Linearity

Non-linear terms in your analysis model present a major challenge in creating an imputation model, because the non-linear relationship between variables can't be easily inverted.

Note: in this example we'll frequently use Stata's syntax for interactions to create squared terms. A varlist of c.x##c.x is equivalent to the varlist x x2 where x2 is defined by gen x2=x^2. The squared term shows up in the output as c.x#c.x. Using c.x##c.x is convenient because you don't have to create a separate variable, and because in that form post-estimation commands can take into account the fact that x and x^2 are not independent variables.

Complete code for this example

Data

Observations: 1,000

Variables:

- x is drawn from the standard normal distribution

- y is x plus x^2 plus a normal error term

Missingness: y and x have a 10% probability of being missing (MCAR).

Right Answers: Regressing y on x and x^2, both should have a coefficient of 1.

Procedure

First, complete cases analysis for comparison:

Source | SS df MS Number of obs = 815

-------------+------------------------------ F( 2, 812) = 1184.66

Model | 2350.4449 2 1175.22245 Prob > F = 0.0000

Residual | 805.533089 812 .992035824 R-squared = 0.7448

-------------+------------------------------ Adj R-squared = 0.7441

Total | 3155.97799 814 3.87712284 Root MSE = .99601

------------------------------------------------------------------------------

y | Coef. Std. Err. t P>|t| [95% Conf. Interval]

-------------+----------------------------------------------------------------

x | .9798841 .0344861 28.41 0.000 .9121917 1.047577

|

c.x#c.x | .9948393 .0244134 40.75 0.000 .9469185 1.04276

|

_cons | -.0047983 .0429475 -0.11 0.911 -.0890994 .0795029

------------------------------------------------------------------------------

The obvious thing to do is to impute x, then allow x^2 to be a passive function of x (it makes no difference whether you create a variable for x^2 using mi passive or allow Stata to do it for you by putting c.x##c.x in your regression). However, this means that the imputation model for x simply regresses x on y. This is misspecified, as you can see from an rvfplot:

Here are the regression results. Because the imputation model is misspecified , the coefficient on x^2 (c.x#c.x) is biased:

Multiple-imputation estimates Imputations = 10

Linear regression Number of obs = 1000

Average RVI = 0.9729

Largest FMI = 0.5328

Complete DF = 997

DF adjustment: Small sample DF: min = 32.79

avg = 37.89

max = 46.68

Model F test: Equal FMI F( 2, 50.2) = 351.77

Within VCE type: OLS Prob > F = 0.0000

------------------------------------------------------------------------------

y | Coef. Std. Err. t P>|t| [95% Conf. Interval]

-------------+----------------------------------------------------------------

x | .9586506 .0570451 16.81 0.000 .8427484 1.074553

|

c.x#c.x | .844537 .0409527 20.62 0.000 .7611974 .9278765

|

_cons | .1986436 .0662195 3.00 0.004 .0654027 .3318845

------------------------------------------------------------------------------

Next impute x using PMM. It's an improvement but still biased:

Multiple-imputation estimates Imputations = 10

Linear regression Number of obs = 1000

Average RVI = 0.3974

Largest FMI = 0.3984

Complete DF = 997

DF adjustment: Small sample DF: min = 56.92

avg = 101.37

max = 134.94

Model F test: Equal FMI F( 2, 167.9) = 763.23

Within VCE type: OLS Prob > F = 0.0000

------------------------------------------------------------------------------

y | Coef. Std. Err. t P>|t| [95% Conf. Interval]

-------------+----------------------------------------------------------------

x | .9511347 .041403 22.97 0.000 .8691019 1.033167

|

c.x#c.x | .9170003 .027871 32.90 0.000 .8618798 .9721207

|

_cons | .1160666 .0565846 2.05 0.045 .0027546 .2293787

------------------------------------------------------------------------------

The include() option of mi impute chained is usually used to add variables to the imputation model of an individual variable, but it can also accept expressions. Does adding x^2 to the imputation for y with (regress, include((x^2))) y fix the problem? Unfortunately not, though it helps:

Multiple-imputation estimates Imputations = 10

Linear regression Number of obs = 1000

Average RVI = 1.1210

Largest FMI = 0.7256

Complete DF = 997

DF adjustment: Small sample DF: min = 17.48

avg = 70.29

max = 118.18

Model F test: Equal FMI F( 2, 39.1) = 377.13

Within VCE type: OLS Prob > F = 0.0000

------------------------------------------------------------------------------

y | Coef. Std. Err. t P>|t| [95% Conf. Interval]

-------------+----------------------------------------------------------------

x | .9629371 .0452655 21.27 0.000 .8727678 1.053106

|

c.x#c.x | .8874316 .0475562 18.66 0.000 .7873051 .9875581

|

_cons | .125851 .053619 2.35 0.021 .0196724 .2320296

------------------------------------------------------------------------------

The imputation model for y has been fixed, but the imputation model for x is still misspecified and this still biases the results of the analysis model. Unfortunately, the true dependence of x on y does not match any standard regression model.

Next we'll use what White, Royston and Wood (Multiple imputation using chained equations: Issues and guidance for practice, Statistics in Medicine, November 2010) call the "Just Another Variable" approach. This creates a variable to contain x^2 (x2) and then imputes both x and x2 as if x2 were "just another variable" rather than being determined by x. The obvious disadvantage is that in the imputed data x2 is not equal to x^2, so it lacks face validity. But the regression results are a huge improvement:

Multiple-imputation estimates Imputations = 10

Linear regression Number of obs = 1000

Average RVI = 0.2375

Largest FMI = 0.3033

Complete DF = 997

DF adjustment: Small sample DF: min = 92.98

avg = 331.43

max = 610.11

Model F test: Equal FMI F( 2, 496.2) = 1330.20

Within VCE type: OLS Prob > F = 0.0000

------------------------------------------------------------------------------

y | Coef. Std. Err. t P>|t| [95% Conf. Interval]

-------------+----------------------------------------------------------------

x | .9905117 .0324469 30.53 0.000 .9267905 1.054233

x2 | 1.005361 .0240329 41.83 0.000 .9580613 1.052662

_cons | -.0018354 .046395 -0.04 0.969 -.0939669 .0902961

------------------------------------------------------------------------------

So would imputing x and x2 using PMM be even better on the theory that PMM is better in sticky situations of all sorts? Not this time:

Multiple-imputation estimates Imputations = 10

Linear regression Number of obs = 1000

Average RVI = 0.3068

Largest FMI = 0.3151

Complete DF = 997

DF adjustment: Small sample DF: min = 86.95

avg = 201.95

max = 312.22

Model F test: Equal FMI F( 2, 163.9) = 1138.59

Within VCE type: OLS Prob > F = 0.0000

------------------------------------------------------------------------------

y | Coef. Std. Err. t P>|t| [95% Conf. Interval]

-------------+----------------------------------------------------------------

x | .9761798 .0346402 28.18 0.000 .9078863 1.044473

x2 | .9987715 .0258422 38.65 0.000 .947407 1.050136

_cons | -.0032279 .0416431 -0.08 0.938 -.0851645 .0787087

------------------------------------------------------------------------------

Lessons Learned

Again, the principal lesson is that misspecification in your imputation model can lead to bias in your analysis model. Be very careful, and always check the fit of your imputation models.

This is a continuing research area, but there appears to be some agreement that imputing non-linear terms as passive variables should be avoided. "Just Another Variable" seems to be a good alternative.

Interactions

Interaction terms in your analysis model also lead to challenges in creating an imputation model because it should take into account the interaction in the model for the covariates being interacted.

Note: we'll again use Stata's syntax for interactions. Putting g##c.x in the covariate list of a regression regresses the dependent variable on g, continuous variable x, and the interaction between g and x. The interaction term shows up in the output as g#c.x.

Complete code for this example

Data

Observations: 10,000

Variables:

- g is a binary (1/0) variable with a 50% probability of being 1

- x is drawn from the standard normal distribution

- y is x plus x*g plus a normal error term. Put differently, y is x plus a normal error term for group 0 and 2*x plus a normal error term for group 1.

Missingness: y and x have a 20% probability of being missing (MCAR).

Right Answers: Regressing y on x, g, and the interaction between x and g, the coefficients for x and the interaction term should be 1, and the coefficient on g should be 0.

Procedure

The following are the results of complete cases analysis:

Source | SS df MS Number of obs = 6337

-------------+------------------------------ F( 3, 6333) = 5435.30

Model | 16167.6705 3 5389.2235 Prob > F = 0.0000

Residual | 6279.30945 6333 .991522099 R-squared = 0.7203

-------------+------------------------------ Adj R-squared = 0.7201

Total | 22446.98 6336 3.5427683 Root MSE = .99575

------------------------------------------------------------------------------

y | Coef. Std. Err. t P>|t| [95% Conf. Interval]

-------------+----------------------------------------------------------------

1.g | -.012915 .0250189 -0.52 0.606 -.0619605 .0361305

x | .9842869 .017752 55.45 0.000 .9494869 1.019087

|

g#c.x |

1 | 1.026204 .0249124 41.19 0.000 .9773671 1.075041

|

_cons | -.0195648 .0177789 -1.10 0.271 -.0544175 .0152879

------------------------------------------------------------------------------

The obvious way to impute this data is to impute x and create the interaction term passively. However that means x is regressed on y and g without any interactions. The result is biased estimates (in opposite directions) of the coefficients for both x and the interaction term:

Multiple-imputation estimates Imputations = 10

Linear regression Number of obs = 10000

Average RVI = 0.5760

Largest FMI = 0.3048

Complete DF = 9996

DF adjustment: Small sample DF: min = 104.17

avg = 130.43

max = 182.89

Model F test: Equal FMI F( 3, 205.4) = 4870.03

Within VCE type: OLS Prob > F = 0.0000

------------------------------------------------------------------------------

y | Coef. Std. Err. t P>|t| [95% Conf. Interval]

-------------+----------------------------------------------------------------

1.g | -.0077291 .0251103 -0.31 0.759 -.0575089 .0420506

x | 1.119861 .0182704 61.29 0.000 1.083631 1.156091

|

g#c.x |

1 | .7300249 .0239816 30.44 0.000 .6827087 .777341

|

_cons | -.0148091 .0174857 -0.85 0.399 -.0494078 .0197896

------------------------------------------------------------------------------

An alternative approach is to create a variable for the interaction term, gx, and impute it separately from x (White, Royston and Wood's "Just Another Variable" approach). As in the previous example with a squared term, the obvious disadvantage is that the imputed value of gx will not in fact be g*x for any given observation. However, the results of the analysis model are much better:

Multiple-imputation estimates Imputations = 10

Linear regression Number of obs = 10000

Average RVI = 0.4359

Largest FMI = 0.3753

Complete DF = 9996

DF adjustment: Small sample DF: min = 69.58

avg = 111.30

max = 210.61

Model F test: Equal FMI F( 3, 223.1) = 5908.62

Within VCE type: OLS Prob > F = 0.0000

------------------------------------------------------------------------------

y | Coef. Std. Err. t P>|t| [95% Conf. Interval]

-------------+----------------------------------------------------------------

x | .9832953 .0159157 61.78 0.000 .9519209 1.01467

xg | 1.018901 .0239421 42.56 0.000 .9713602 1.066443

g | -.0141319 .0247797 -0.57 0.570 -.0635346 .0352709

_cons | -.0087754 .0176281 -0.50 0.620 -.0439374 .0263866

------------------------------------------------------------------------------

Another alternative is to impute the two groups separately. This allows x to have the proper relationship with y in both groups. However, it also allows the relationships between other variables to vary between groups. If you know that some relationships do not vary between groups you'll lose some precision by not taking advantage of this knowledge, but in the real world it's rare know such things.

Multiple-imputation estimates Imputations = 10

Linear regression Number of obs = 10000

Average RVI = 0.3627

Largest FMI = 0.3482

Complete DF = 9996

DF adjustment: Small sample DF: min = 80.48

avg = 218.72

max = 369.37

Model F test: Equal FMI F( 3, 456.6) = 6783.26

Within VCE type: OLS Prob > F = 0.0000

------------------------------------------------------------------------------

y | Coef. Std. Err. t P>|t| [95% Conf. Interval]

-------------+----------------------------------------------------------------

1.g | -.0218404 .0243087 -0.90 0.372 -.0702117 .0265309

x | .9869436 .0156451 63.08 0.000 .9561207 1.017766

|

g#c.x |

1 | 1.018534 .0214947 47.39 0.000 .976267 1.060802

|

_cons | -.0076746 .0158825 -0.48 0.629 -.0390027 .0236534

------------------------------------------------------------------------------

Lessons Learned

Once again, the principal lesson is that misspecification in your imputation model can lead to bias in your analysis model. Be very careful, and always check the fit of your imputation models.

This is also an area of ongoing research, but there appears to be some agreement that imputing interaction effects passively is problematic. If your interactions are all a matter of variables having different effects for different groups, imputing each group separately is probably the obvious solution, though "Just Another Variable" also works well. If you have interactions between continuous variables then use "Just Another Variable."

Acknowledgements

Some of these examples follow the discussion in White, Royston, and Wood. ("Multiple imputation using chained equations: Issues and guidance for practice." Statistics in Medicine. 2011.) We highly recommend this article to anyone who is learning to use multiple imputation.

Next: Recommended Readings

Previous: Estimating

Last Revised: 6/21/2012